Felix — Software Engineer | Digital Transformation Consultant March 2026

I Use AI Every Day. And I Don't See the Money.

I'm going to start where nobody in this industry wants to start: with the bottom line.

I'm a software engineer with over ten years of experience. I use Claude, ChatGPT, Copilot — all of it. AI is part of my daily workflow and my team's. Does it make us more productive? Absolutely. Does it show up in revenue? No. What does show up every month, right on time and crystal clear, is the expense. The subscriptions. The tokens. The invoice. The return is a different story — fuzzy, impossible to attribute to a specific client or project.

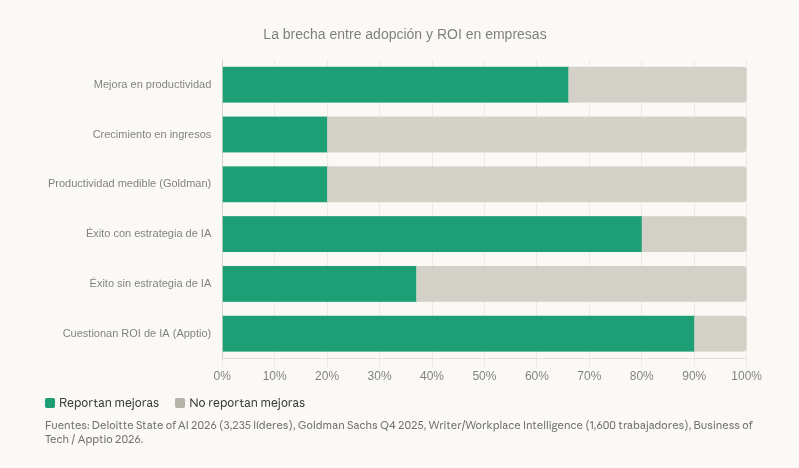

Turns out I'm not an isolated case. Deloitte surveyed over 3,200 business leaders in 2025: 66% say AI improved their productivity, but only 20% — one in five — report actual revenue growth. The remaining 74% classify it as a "future aspiration." A polite way of saying the check hasn't arrived.

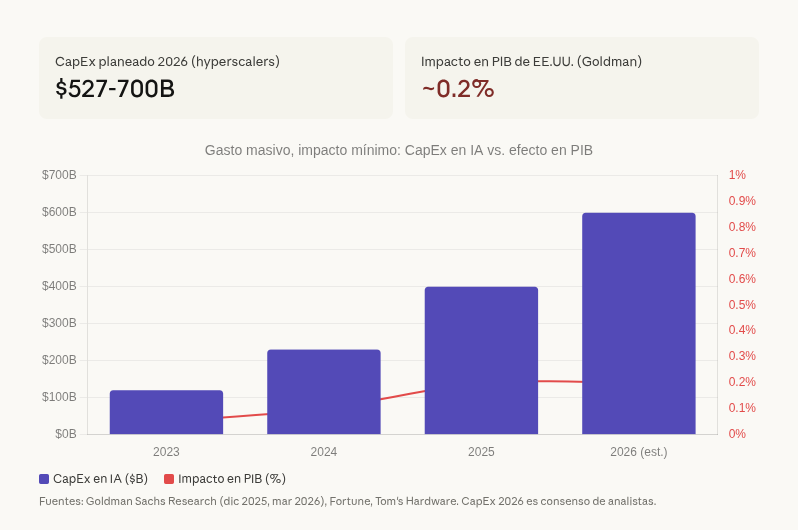

Goldman Sachs put a number on what many of us suspected: the impact of all AI investment on U.S. GDP in 2025 was, in the words of chief economist Jan Hatzius, "basically zero." This with $700 billion planned for 2026 in infrastructure alone.

How is it possible to spend so much and move so little? That's the question that led me to write this. Not as a critique of the technology — which I use and value — but as an analysis of why most companies are adopting it wrong.

The Arms Race

There are two ways to spend money: because you expect to earn more, or because you're afraid of losing what you have. The AI industry today operates almost exclusively on the latter.

Microsoft didn't put $13 billion into OpenAI because Excel with Copilot was going to triple its revenue. It did it because if Google cracked AGI first, Microsoft would become irrelevant within a decade. Amazon poured $4 billion into Anthropic, conveniently structured as an AWS infrastructure investment. Google accelerated Gemini while laying off thousands of employees. Meta open-sourced Llama — not out of generosity, but to commoditize everyone else's models and protect its platforms given its initial inability to compete.

None of those decisions came from a spreadsheet with positive ROI. They're expensive insurance policies against a future no one can predict.

That logic replicated across the entire economy. The mid-size company adopting AI isn't doing it because it calculated a 15% return. It's doing it because its competitor adopted it and it can't afford to fall behind. It's the prisoner's dilemma: everyone spends, no one can stop, and the net benefit is marginal for all.

Buying weapons isn't profitable in itself. There's no ROI. But being unarmed when everyone else is arming up can be fatal. That's how AI investment works today.

Neha Khoda, a Bank of America analyst, summed it up well: AI has entered its "show me" phase — where big numbers no longer impress unless they come with real results.

The Numbers Behind the Curtain

Let's look at the financials of the most relevant AI labs. Not the ones they put in press releases — the real ones.

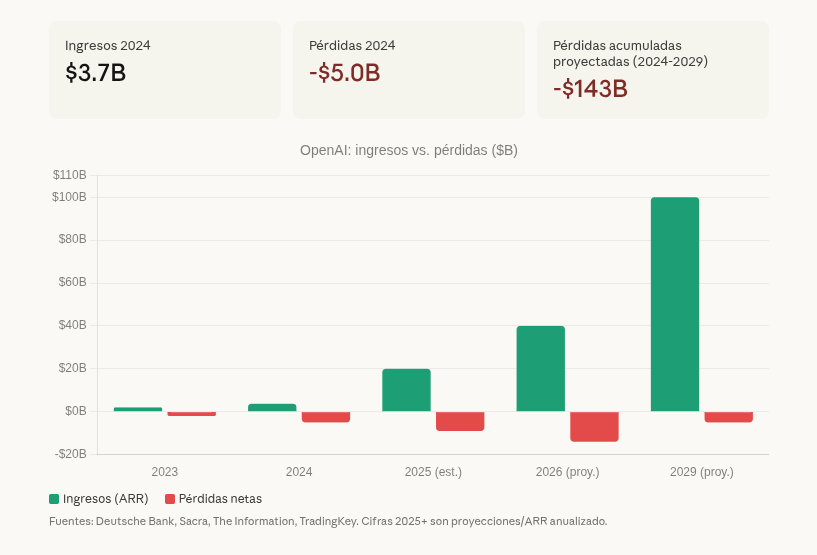

OpenAI generated $3.7 billion in revenue in 2024. It lost $5 billion. Read that again: it spent $2.25 for every dollar it earned. By 2025, ARR climbed to around $20 billion — impressive growth — but the cash burn was $9 billion. Deutsche Bank projects $143 billion in cumulative losses before OpenAI reaches profitability, something they don't expect before 2029. Paul Kedrosky put it in simple terms: "They're selling dollars for 70 cents wholesale."

In November 2025, OpenAI launched an ad-supported free tier. They're also considering adult content. When a company goes from a non-profit founded to "ensure AI benefits all of humanity" to pivoting toward ads and adult content in six years, that's not a strategic pivot. That's looking for money under the couch cushions.

Anthropic has grown remarkably: from ~$1 billion in ARR at the end of 2024 to $14 billion by February 2026. It closed a $30 billion round at a $380 billion valuation. But it burned $5.6 billion in 2024, projects $3 billion in 2025, and faces $80 billion in cloud infrastructure costs through 2029. It projects positive cash flow by 2027. It has better metrics than OpenAI — generating $2.10 per compute dollar versus OpenAI's $1.60 according to Fortune — but the underlying dynamic is the same: massive growth funded by investment rounds while chasing profitability.

The other labs face variations of the same problem. Google subsidizes Gemini with ad revenue. Meta funds Llama with its social media business. Nobody is generating direct returns from the AI business itself.

The central paradox: the more they sell, the more they lose. Compute costs grow as fast as revenue or faster. This isn't a scale problem. It's a structural one.

China and Open Source Are Coming for the Margins

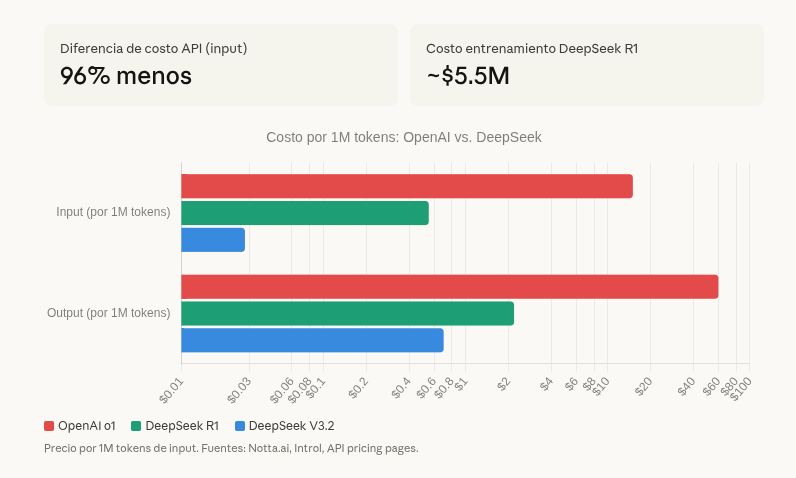

DeepSeek, a Chinese lab, trained its R1 model for roughly $5.5 million, using GPUs inferior to what any American big tech company has. The result: performance comparable to OpenAI's o1 model. Its API costs 96% less — $0.55 per million input tokens versus $15 from OpenAI.

96% less. For a product that's equivalent on many benchmarks.

Meta keeps improving Llama as open source. Qwen (Alibaba) is advancing. Mistral is closing the gap. Every time an open model matches a paid one, the justification for charging a premium weakens. And the cycles are getting shorter — a new model's advantage lasts months, not years.

SemiAnalysis notes that DeepSeek's real cost is higher when you include infrastructure and R&D — roughly $1.6 billion in total server CapEx. But the optimization techniques they developed are available for anyone to adopt. Efficiency, once discovered, can't be undone.

If a competitor can offer 95% of the performance at one-tenth the price, how long can you charge a premium? Less than you think.

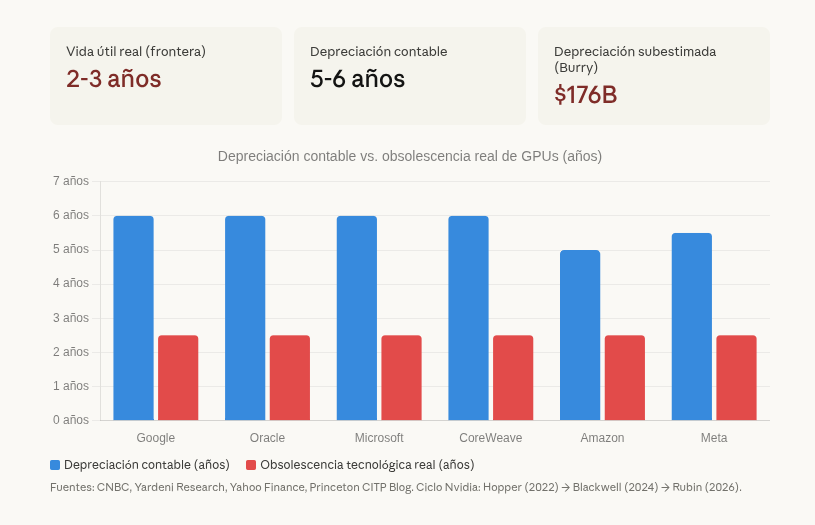

The Hardware Rots Faster Than It's Paid Off

This is the least discussed point and the one that should concern you the most.

AI data centers aren't buildings you depreciate over 30 years. Nvidia's GPUs have a useful life on the technological frontier of 2 to 3 years. Nvidia has already shifted to an annual product cycle: Hopper (2022), Blackwell (2024), Rubin (2026). Each generation makes the previous one lose competitiveness rapidly — Blackwell offers up to 25 times better energy efficiency than Hopper for certain inference tasks.

Yet Google, Oracle, and Microsoft depreciate those same chips on their books over 5-6 years. Michael Burry — the investor who predicted the 2008 crisis — estimates that this discrepancy could represent $176 billion in understated depreciation between 2026 and 2028. Artificially inflated profits.

Satya Nadella, Microsoft's CEO, admitted he didn't want to "get stuck with four or five years of depreciation on a single generation." When the CEO of the company that spends the most on AI says that publicly, the message is clear: even the biggest buyers are nervous about how fast their investment loses value.

Without sustainable cash flow, how do AI labs plan to maintain their infrastructure? They need to raise capital permanently just to replace hardware that becomes obsolete every two years. It's a hamster wheel.

The Democratization Paradox

This is the argument I consider the strongest and the least discussed.

Let's assume the best-case scenario. AI delivers on all its promises. Models become extraordinary. Costs drop. Everything works. What happens?

AI destroys the competitive advantages of the very companies paying for it.

A concrete example. Someone with a PC, a good AI model, patience, and creativity could recreate functionality equivalent to Photoshop. Or any Adobe product — one of the most anti-consumer companies in tech. Adobe goes from competing against two or three companies to competing against all of humanity. Multiply that across every software category: CRM, ERP, analytics, project management.

Nvidia sells chips so companies can use AI. That AI enables small competitors to replicate those companies' products. The companies lose revenue, cut their AI spending, and Nvidia loses too. The chain devours itself.

It's like selling weapons to every side of a war at the same time. Great business at first. Unsustainable in the end.

The better AI gets, the worse the investment case for those funding it. If models are mediocre, big tech maintains its edge. But if AI actually works, anyone can compete with anyone, and margins collapse across the entire industry. According to Andreessen Horowitz, 81% of companies already use three or more model families in production — competition among providers is eroding margins in real time.

So, What Do We Do?

Right now there's no magic formula. But after using AI daily and advising companies on digital transformation, there are clear patterns that separate those getting value from those throwing money away.

Admit you're spending out of fear. If the main reason you adopted AI is "because the competition did," that's not strategy — it's panic. Define what specific problem it solves, how you'll measure the impact, and what success looks like. Data from Writer/Workplace Intelligence: companies without a formal AI strategy report 37% adoption success. Those with one: 80%. The difference isn't the technology. It's having a plan.

Change how you charge. If AI lets you do in 2 hours what used to take 20, the billable hours model self-destructs. Charge for outcomes, for value delivered, for problems solved. If you don't change the business model, AI will just make you work faster for less money.

Understand that your edge isn't the tool. As models commoditize (and they will), differentiation shifts to who knows how to apply them best. Nobody pays a premium for electricity, but the companies that leveraged it best built empires. Your domain expertise, your client relationships, your ability to execute — that's what's valuable.

Don't marry a single provider. Those charging a premium today may be commodity tomorrow. Stay flexible.

This Isn't Science Fiction. It's Accounting.

I'm not anti-AI. That would be absurd — I use it all day and believe it has transformative potential. Electricity was real in 1890. The internet was real in 1999. Both technologies changed the world. And in both cases, many of the companies that went all-in at the wrong time went bankrupt before seeing the benefits.

The risk isn't that AI fails. It's that the market does to it what it did to the internet in 2001 — kills the momentum with a correction that freezes investment right when we were close to the real breakthrough.

Goldman Sachs found that where impact is actually measured on specific tasks, productivity gains are around 30%, concentrated in software development and customer service. The potential is there. But it won't materialize by throwing money at the problem with your eyes closed.

The companies that will win with AI aren't the ones that spend the most. They're the ones that spend the smartest. And that starts with stopping fear-driven investment and starting to invest with intention.

Is Your Company Investing in AI Intelligently?

Answer 12 questions in 2 minutes and receive a free diagnostic with personalized recommendations for your company.

Felix is a software engineer with over 10 years of international experience in modern web architectures (Next.js, NestJS, Node.js, PostgreSQL, AWS). He co-founded a strategic consulting firm focused on digital transformation. He uses AI tools daily in his work.

References

Reports and surveys Deloitte, "State of AI in the Enterprise 2026" — 3,235 leaders (Aug-Sep 2025) | Goldman Sachs Research — AI impact on GDP (Q4 2025 / Q1 2026) | Andreessen Horowitz, "Enterprise AI arms race" (Feb 2026) | Menlo Ventures, "State of Generative AI" (Dec 2025) | Writer / Workplace Intelligence, "2025 AI Adoption Report" — 1,600 workers | NVIDIA, "State of AI 2026" — 3,200+ respondents | PwC, "2026 AI Predictions" | Lucidworks, "Enterprise AI in 2026" — 1,600+ leaders

Financial analysis Sacra — OpenAI and Anthropic (Mar 2026) | Deutsche Bank — OpenAI losses $143B (Dec 2025) | TradingKey (Jan 2026) | DigiDAI (Mar 2026) | European Business Magazine (Feb 2026) | Fortune / Goldman Sachs capex vs. profit (Jan 2026)

Depreciation and hardware CNBC — GPU depreciation (Nov 2025) | Yahoo Finance (Dec 2025) | Stanley Laman Group | Princeton CITP Blog (Oct 2025) | Yardeni Research (Nov 2025)

Competition and costs Introl — DeepSeek V3.2 (Dec 2025) | Notta.ai — DeepSeek R1 vs o1 | SemiAnalysis (Jan 2025) | Om Malik (Feb 2026)